This newsletter has been supported by ListedReserve, a fund manager focused on digital assets. While we do not focus on this space, we strongly appreciate the insights of a manager immersed in the area, and thoroughly enjoy reading their newsletter.

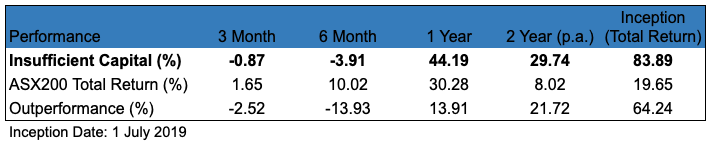

Key team members have recently graduated university and begun new roles – Peter is now a Portfolio Manager at Waterhouse VC, whilst Matthew is a buy side research analyst within a trading firm. Consequently, the portfolio has slightly shifted towards an increased allocation to passive investments: 13% is invested across two ETFs (focused on global equities ex-Australia) and 13% is invested across two LICs (focused on ‘value’ equities, particularly mining and energy). We will touch on the LICs in a future newsletter and discuss why they could outperform the index. Earlypay (EPY:ASX) is our largest position, with the top 3 positions currently representing 36% of the portfolio.

We will periodically discuss changes to the direct equity positions. Recent portfolio additions include: Dusk (DSK:ASX), Charter Hall Long WALE REIT (CLW:ASX), Allegiance Coal (AHQ:ASX) and Earlypay (EPY:ASX). We trimmed 10% of our Smartpay (SMP:ASX) position at $0.72 to rebalance the portfolio.

Cracks in the US economy are beginning to emerge.

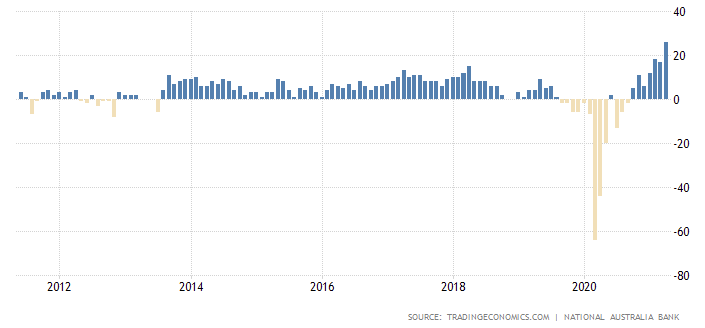

The ‘Loan Officer Survey’ asks banks if it is easier or more challenging to give new loans. This survey is a barometer for the US economy, with implications for credit availability. The recent upward movement (see the red line) indicates that it is becoming more challenging and that there is a high risk of widening credit spreads. Check out the prior three spikes (2001, 2008/2009, 2020) in both credit standards and the US HY Credit Spread – these were not great times for US consumers or equity investors.

Walmart and Target both reported disastrous earnings, citing inflationary pressures on American households. Over the following days, Walmart closed down 11.4%, its worst day since October 1987 and Target fell 25% on their posted earnings. The US market is increasingly appearing fragile – in mid-May, Snapchat cited macroeconomic pressures as negatively influencing their recently published guidance.

Even cryptocurrencies – favoured as a historically ‘uncorrelated’ asset class that is characteristically higher risk (and higher reward), has had its risk-off moment. The total market capitalisation of cryptocurrencies has fallen from $3T to $1.2T today, headlined by the collapse of Terra’s LUNA and TerraUSD (UST) – an event likely to be cited in economics textbooks for years to come.

The Fed is tightening into this negative backdrop. This is very different to March 2020. The lifesaver of the US consumer is reeling back its rafts.

MoneyBits is the crypto newsletter for investors (not naysayers).

Every Friday, Dan (ListedReserve’s founder) sends a newsletter on the fundamentals of the sector.

Yep, the fundamentals. Forget about bored apes and dog coins. It keeps us focused on the opportunities, and sceptical of the hype.

It’s trusted by top fund managers, VCs and wealth advisors too. Oh, and it’s free.

If you’d like to give it a try click here.

RPM Automotive

RPM Automotive (RPM) was founded by Clive Finkelstein (CEO and Managing Director) and Lawrence Jaffe (Executive Director) in 2013, as a group of diversified automotive businesses offering customers: tyres for commercial and passenger vehicles, vehicle servicing & repairs, roadside assistance, motor accessories, and motorsport safety gear.

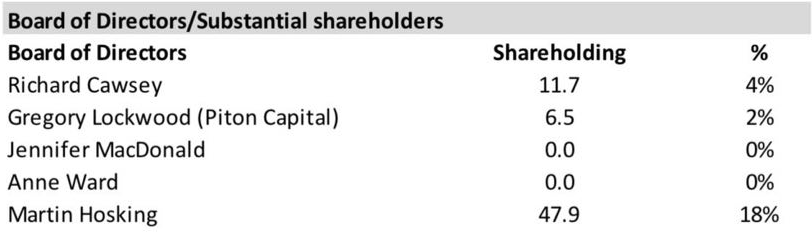

The company’s strategy encompasses both organic and inorganic growth, with acquisitions aimed at valuations of 3.5-5x EBITDA using around 50% scrip and 50% cash consideration. RPM applies a term payout to retain vendors in the business for 3+ years, with escrow applied to the scrip consideration. Original vendors of businesses acquired by RPM currently own 17% of the $50 million company.

Clive and Lawrence remain significant shareholders, owning 14% of the company each. Clive is an industry veteran, having previously built and sold a parts and accessories manufacturer as well as a wholesaler and a 4WD franchise. We have a strong preference for investing in founder-led businesses. Founders typically have comprehensive knowledge, moral authority, and full commitment to a long-term vision rather than quarterly earnings.

In August 2021, RPM secured $8m of growth funding from Collins St Value Fund, which is a high performing Melbourne-based fund (returned 19.1%pa since inception). Collins St invested $2.5m in RPM at 30c and provided a 3-year $5.5m convertible note convertible at 35c with a 3.5% coupon. At the base of this newsletter, we have linked an interview with Michael Goldberg, Collins St’s Managing Director, where he discusses RPM.

In April, RPM’s management upgraded guidance for the financial year:

| Metric | Upgraded Guidance | Prior Guidance |

| Revenue ($m) | 80-85 | 78 |

| EBITDA ($m) | 7.2-8.2 | 7+ |

We estimate that the business will generate around $3.1m of NPAT in FY22 and $5.5m+ of NPAT in FY2023. At a market capitalisation of $50m, the business is currently valued at circa 16x FY22 PE / 9x FY23 PE. Taking the middle of guidance, RPM trades at 5.9x EV/EBITDA – however, we care far more about cash flows than EBITDA for a business like RPM.

On an EV/EBITDA basis, RPM is far cheaper than ASX-listed peers, although it is undoubtedly subscale compared to them and certainly deserves a lower valuation multiple than ARB Corporation.

| Company | Enterprise Value ($m) | FY2022 Forecast EBITDA ($m) | FY2022 Forecast EV/EBITDA |

| ARB Corporation (ASX:ARB) | 2,550 | 196 | 13.0x |

| Bapcor (ASX:BAP) | 2,550 | 288 | 8.9x |

| Carbon Revolution (ASX:CBR) | 74 | -27 | n/a |

| National Tyre and Wheel (ASX:NTD) | 219 | 15 | 14.4 |

| PWR Holdings (ASX:PWH) | 804 | 35 | 23.0 |

| RPM Automotive (ASX:RPM) | 45.2 | 7.7 | 5.9x |

RPM is clearly leveraged to the discretionary income of Australian consumers. We continue to monitor for the deterioration of economic conditions both globally and domestically, especially consumer spending, inflation and widening credit spreads. Representing 26% of group revenue, RPM’s ‘Motorsport’ and ‘Performance and Accessories’ divisions are particularly leveraged to discretionary spending.

In saying that, we are not macro strategists but mere stock pickers. Considering the operational expertise of RPM’s founders, the company’s strong balance sheet (net cash of $3.8m) and compelling valuation, as well as its long growth runway, we are happy to join Clive on his three-year plan for $150m+ of group revenue.

Quip of the Month

“Many fail to grasp what they have seen, and cannot judge what they have learned, although they tell themselves they know.” – Heraclitus (Greek philosopher of the late 6th century BC)

The Dunning-Kruger Effect is a type of cognitive bias where people overestimate their competence in one or several fields. Essentially, low ability people do not possess the skills needed to recognise their own incompetence!

The Dunning-Kruger Effect. Source: MedicineNet

The Dunning-Kruger Effect is certainly prevalent in public markets, where alpha is incredibly difficult to find. 83.1% of active funds have underperformed compared to the S&P500 over the last 10 years and underperformance rates around 80% have been recorded across the developed world. Such a damning statistic does not exactly exude confidence or encourage active management.

Anyone with a small pool of capital can compete to efficiently price public equities. Many people are incredibly bright and/or industry experts, with easy access to rich data points (such as website traffic data through Similarweb and unique business insights through Tegus) and powerful analysis tools such as CapIQ, Bloomberg and Sentieo. As technological capability and availability have increased over the last 50 years, the relative skill gaps between investors have narrowed significantly. We could not possibly know more about Facebook or CSL (pick any large cap) than anyone else and it would be a textbook example of the Dunning-Kruger Effect.

We have gradually realised that we must hunt where the rest of the world is not. Doing so in Australia, a country that only represents 1.03% of the global market is a great place to start. As of February this year, there are 2145 Australian public companies, of which, around 1850 (those outside the ASX300) have a market capitalisation below $800 million.

Global stock exchanges by market capitalisation as of December 2021. Source: Statista

For our large cap exposure, we generally prefer to own ETFs. We could feasibly gain an information edge over the rest of the market in smaller companies like RPM Automotive… although perhaps this too is putting the Dunning-Kruger Effect to practise.

Australian mid- and small-cap funds have fared much better than large-cap funds, with a slim majority outperforming their benchmark over most time frames. 51.2% have outperformed over the past 15 years.

Source: SPIVA

Larger and more developed markets, like the US, have much greater efficiency for mid- and small-caps. Perhaps it’s time for you to review any actively managed US exposure…

Source: SPIVA

Extraordinary outcomes are very unlikely to be achieved through ordinary actions. Small companies like RPM are likely to drive our entire outperformance… if we are fortunate enough to avoid the Dunning-Kruger Effect, and a myriad of other exciting obstacles.

If you would like further details regarding our activities, we encourage you to follow us on Twitter, where we share more regular bite-sized commentary. Email us at insufficientcapital@gmail.com.

See Michael Goldberg discuss the ‘special sauce’ of founder-led businesses, with specific reference to RPM here.

Kind Regards,

Insufficient Capital