Happy Holidays to all our subscribers. Thank you for your support throughout our first half year – we greatly appreciate it and wish you many happy returns in the New Year. Hopefully we can help with some of those financial goals (but keeping the New Year gym membership resolution is not our responsibility). We encourage you to review our website, and follow us on Instagram and Twitter, where we share more regular bite-sized commentary.

Buckle up. This is an end of year special. The structure of this newsletter:

- Performance figures

- Podcast with Frazis Capital

- What went wrong this past half year at Insufficient Capital

- What went right this past half year at Insufficient Capital

- Stock focuses on Afterpay (APT:ASX) and Acrow Formwork (ACF:ASX)

- 5 stocks on our 2020 watchlist (we will provide details on 5 more watchlist stocks in the next newsletter)

Performance Figures

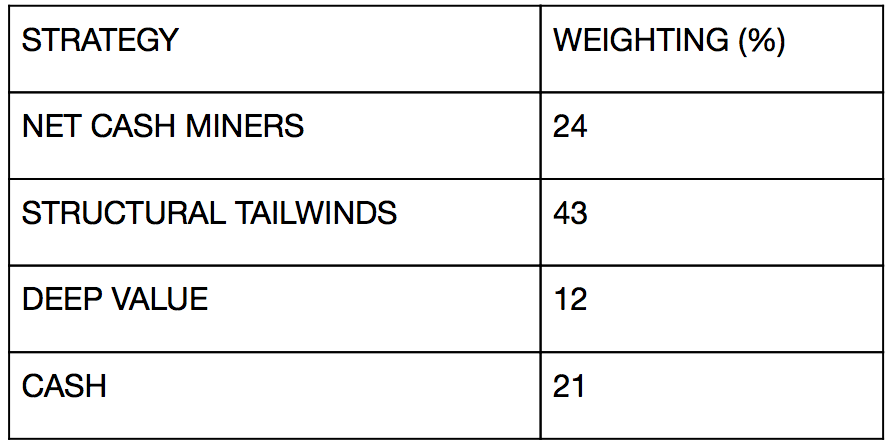

At the end of the December quarter, the fund was most heavily weighted to our ‘Structural Tailwinds’ strategy. ‘Structural Tailwinds’ refers to areas of the economy which are growing at a faster rate than the national average growth rate. Afterpay is our largest holding:

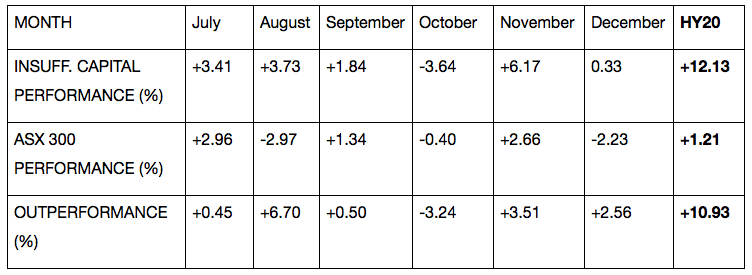

The portfolio rose +2.65% over the quarter, outperforming the ASX300 performance of -0.03% by +2.68%. The top contributor during the quarter was Acrow Formwork (ACF:ASX) while the largest detractor was Stanmore Coal (SMR:ASX). The top contributor during December was Stanmore Coal (SMR:ASX), while the largest detractor was Afterpay (APT:ASX). The fund currently holds 21% cash.

It was very pleasing to report outperformance of +10.93% over the half year, with outperformance over all months but October. This puts the portfolio well on track to achieve its outperformance target of +10%/annum above the ASX300. The cash position held over the half year averaged 22% while the position in gold (typically defensive) averaged 10%. Outperformance has been achieved through this relatively conservative exposure. The majority of our portfolio holdings have net cash on their balance sheets, ensuring the overall portfolio remains financially secure and nimble. This is particularly important during the current seemingly never-ending bull market, where the cost of domestic credit continues to break record lows. The fund continues to keep an eye on, but remains relatively indifferent to, macroeconomic conditions.

Put simply, we find businesses that we like, and we buy them throughout the cycle.

As far as the peak of the business cycle is concerned, Warren Buffett addresses the matter far better than we could:

“In the 20th Century, the United States endured two world wars and other traumatic and expensive military conflicts; the Depression; a dozen or so recessions and financial panics; oil shocks; a flu epidemic; and the resignation of a disgraced president. Yet the Dow (Jones Index) rose from 66 (points) to 11497 (points).”

Podcast with Frazis Capital

We recently thoroughly enjoyed recording a podcast with Frazis Capital Partners. Check out Part 1 (Part 2 will be in the next newsletter) of the discussion on growth opportunities and the software sell-off on desktop here and on iTunes here. Frazis Capital invests in a high conviction global portfolio focused on technology and the life sciences. The fund is one of the few investment vehicles in Australia focusing entirely on technology and the life sciences. Many value managers actively avoid these sectors. Michael (portfolio manager) has a deep understanding of the intricacies of the life sciences, having read chemistry at Oxford. Unlike Insufficient Capital, Frazis Capital is open for investment. The fund has posted a very strong performance of +29% this calendar year to date (as of 30 November).

What Went Wrong this Half Year at Insufficient Capital

Despite the significant outperformance recorded, there were a couple of disappointing outcomes throughout the half year. The largest stock-specific mistake concerned our largest position at the start of the half year, Stanmore Coal (SMR:ASX). There is always commodity price risk in miners. We entered the position, attracted by Stanmore’s strong margins, cashed up balance sheet (no debt), higher quality product, experienced management and project pipeline, concluding that the company could weather a coking coal price downturn.

The coking coal price has collapsed from a peak of $200/tonne in May 2019 to $140/tonne today:

Despite the price fall effectively halving Stanmore’s profit margin, the stock was supported well into September by a prospective buyout proposal from Winfield Group Investments for $1.50-$1.70/share.

We formed the opinion that despite the falling coking coal price, other bidders were likely to emerge, attracted to the firm’s vast free cashflows and deleveraged balance sheet. Less than a year ago, Stanmore had received a buyout offer from Golden Investments, a potential rival bidder against Winfield.

Stanmore Coal Equity:

At its peak, with the offer still in play, Stanmore had expanded to over 20% of the fund’s assets. Internally, we have a target valuation of around $1.90/share, with a belief that Stanmore is undervalued (a 40% discount to its larger peers) considering its high quality coking coal (rather than thermal coal) assets and net cash balance sheet.

In short, the buyout fell through because the other major shareholders refused to cooperate (M Resources and Golden Investments) and no further bids were received. The stock corrected >30% to adjust for the lower coking coal price, costing us >6%. In hindsight, despite the fund’s internal valuation of $1.90/share, the position should have been halved to a circa 10% weighting. $1.50-$1.70 was the offer on the table and Insufficient Capital is not in the business of merger arbitrage. Lesson Learnt.

A firm pillar of the Insufficient Capital investment methodology is buying and holding investments, effectively letting the market rebalance the portfolio over time (provided the investment thesis remains unchanged). For example, a portfolio of 10 stocks bought today with a 10% weighting in each stock, will have vastly different weightings if no changes are made over the ensuing 2-5 years. After such an extended period of time, it is quite likely that the largest 3 holdings account for over 60% of net assets, while the smallest 3 account for less than 15%. Our philosophy had not been tested by a prospective buyout. We were offered a multi-week opportunity to exit at an M&A elevated valuation after the coal price had collapsed… the benefits of hindsight.

It is now back to business as usual. Stanmore will likely generate over $100M of EBITDA this financial year and EPS of circa $0.25, with earnings supported by continued global stimulus driving steel-making across Asia. The market values Stanmore at a forward PE of 4X and EV/EBITDA of 1.6X. The firm continues to trade at a 40% discount to a basket of its peers despite its superior quality coal and substantial cash position. The main reasoning behind the ‘Net Cash Miners’ strategy is continual investment throughout the cycle (particularly when commodity prices are depressed) and resilience to the threats of cyclical downturns. Cash also facilitates asset purchases at heavily depressed valuations. It is important to remember that Stanmore transformed a $1 asset purchase (when coking coal prices were low in 2015) into a $300M company.

The other key mistake made during the half year concerned general issues around position sizing. As described above, setting and forgetting a portfolio for a long period will always show a portfolio manager which companies are performing well because “In the short run, the market is a voting machine but in the long run, it is a weighing machine” (Benjamin Graham). Going forward, we will be much stricter on initiating every new position at a similar size (weighted relative to risk), resisting the urge to add to positions or transact without high conviction. At the moment, Insufficient Capital transacts around twice per month (this is quite low but could be decreased considering our ‘buy and hold’ mentality).

What Went Right this Half Year at Insufficient Capital

Consolidating the fund’s overall strategy in April has been successful thus far. Paying a fair price for great core businesses through fundamental analysis has been the key to success. Analysing businesses’ future cashflows and future cashflows alone is what we do best. All other methods of valuation are background noise.

The top three contributors which account for approximately all of the fund’s performance over the half year are:

- EML Payments (+6.5%)

- Afterpay (+3.6%)

- Pointsbet (+2.5%)

Whilst a high level of consolidation amongst performance contributors is expected for a high conviction portfolio, underperforming holdings in the portfolio must have their time in the sun. This is the only way to sustain long term outperformance without high volatility since outperforming holdings which continue to outperform will increase in portfolio weighting, and thus, potential drawdown. We believe that Acrow Formwork (see further analysis below) will be the most likely outperformer out of the fund’s previously underperforming holdings.

Stock Focus: Afterpay (APT:ASX)

Afterpay is one of the most widely discussed stocks on the Australian market. In fact, the fund’s sources reveal that it has become very topical amongst US investment circles (particularly after US technology fund, Coatue Management, invested $200M in November). It is difficult to add a different perspective to Afterpay but hopefully the commentary below adds value to the overall picture. Some of our prior commentary on Afterpay can be found in the August newsletter.

The fund believes this is an excellent time to own Afterpay stock, with exponentially increasing spend/customer and superb execution in the US, where the overall customer count is now comparable to Australia. The August newsletter highlighted the relationship between domestic purchasing frequency and time since joining Afterpay. This year’s annual results (reported 28 August) revealed that customers for 3+ years purchased through Afterpay around 20X/annum, 2+ years around 10X/annum and 1+ years around 4X/annum. Those customer cohorts now respectively spend 22X/annum, 14X/annum and 7X/annum.

It is important to remember that nearly all of the circa 3 million US customers fall into the 7X/annum category (along with the >500K UK customers added since launch 8 months ago). If the overseas customers follow Australian consumer behaviour, total purchases across the entire business could more than double over the next 2 years. That is without any further customer acquisition or increased domestic purchasing frequency.

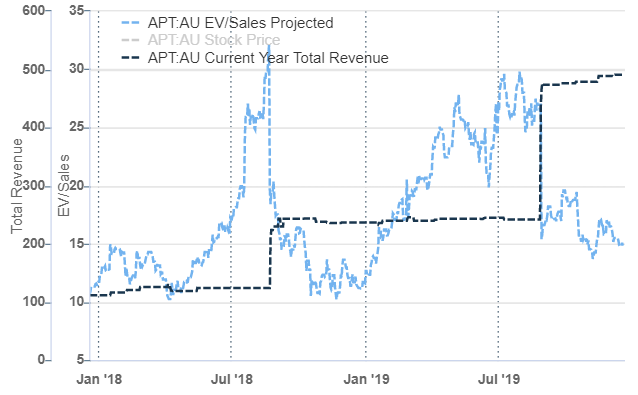

Afterpay is currently trading at around 15X forward EV/Sales, towards the lower end of its historical trading range (however, as described above, we place little value on historical trading ranges). In the past, Afterpay has traded between 10X forward EV/Sales and 30X forward EV/Sales (30X usually prior to the announcement of annual results in August). By the end of this financial year (June 30, 2020), Afterpay will be far more established in the US and UK. Strong underlying sales growth is again expected over this financial year (underlying sales grew +140% last financial year), driven by customer growth in the US and UK along with increases in spend/customer across all markets… the black revenue line should significantly leg up again come next year:

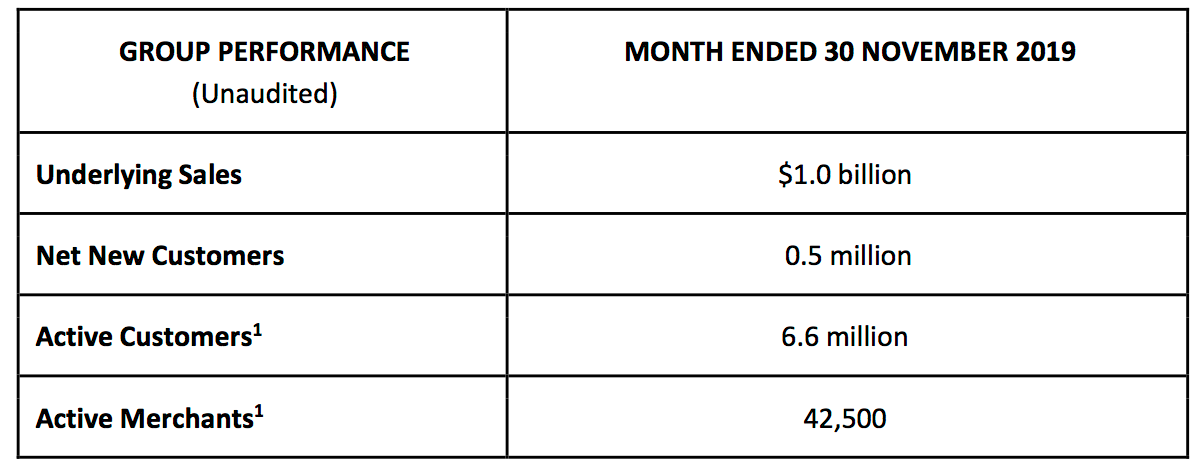

November’s sales figures boded very well for FY2020 revenue, driven by record sales on Black Friday and Cyber Monday. The $1B of sales processed by Afterpay was a monthly record for the company. Sales of $160M over Black Friday and Cyber Monday were up +160% compared to last year. Afterpay also attracted over 140,000 new customers over the 2 days. The business is on track to process over $9B of sales this financial year (FY2019 recorded $5.2B of sales).

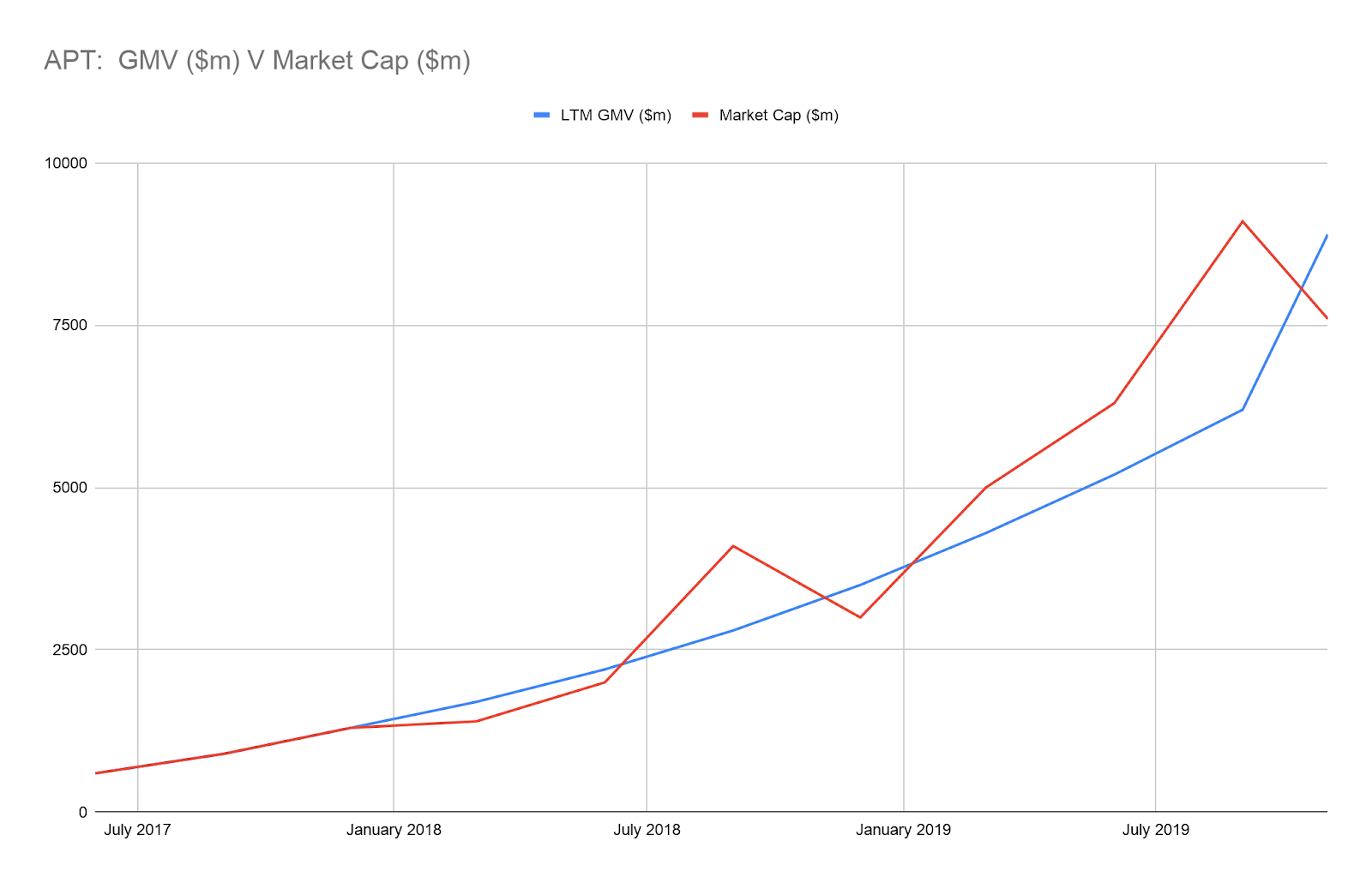

Gross Merchandise Volume (GMV – effectively equivalent to total underlying sales for Afterpay) and the company’s market capitalisation have both increased significantly over the last 2 years:

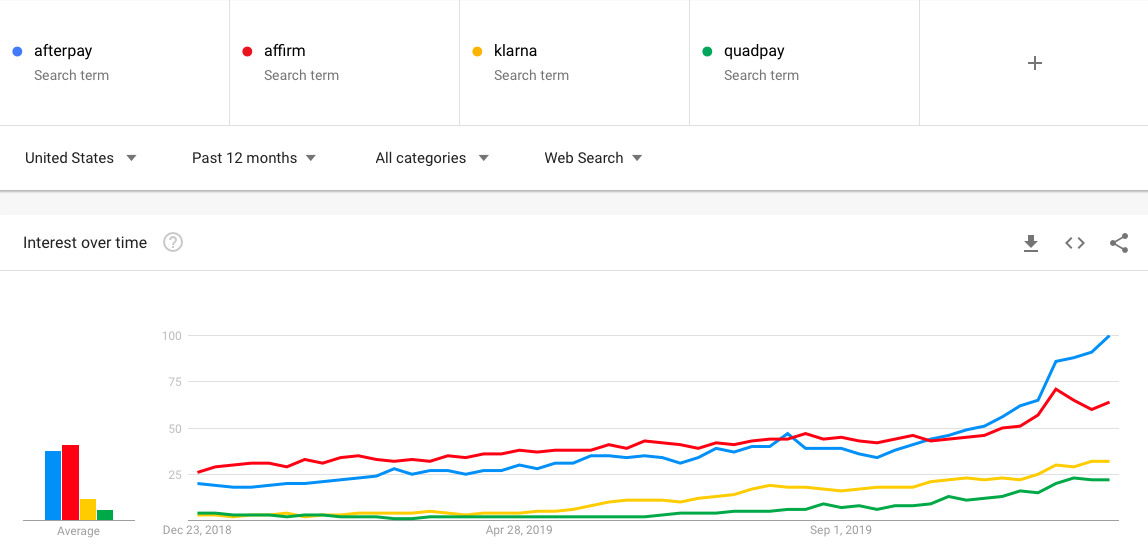

We have tracked interesting measures for Afterpay’s development: Instagram follower growth, google trends data and iOS app ratings. The graph below illustrates the growth of the google search term, “Afterpay”, compared to its 3 largest US competitors. Afterpay is clearly gaining superb traction in the US, with google search frequency increasing about 5X over the last 12 months:

Despite the stock appreciating over 5X since our first entry, we have never been more excited about Afterpay’s future prospects. We are confident that it will still be our largest holding at the end of the financial year.

Stock Focus: Acrow Formwork (ACF:ASX)

Acrow Formwork is typical of Insufficient Capital’s ‘Deep Value’ strategy. The companies in this category are unloved, often relatively unknown operating businesses that produce strong cashflows. The thesis behind Insufficient Capital’s initial investment in Acrow can be found in an earlier newsletter.

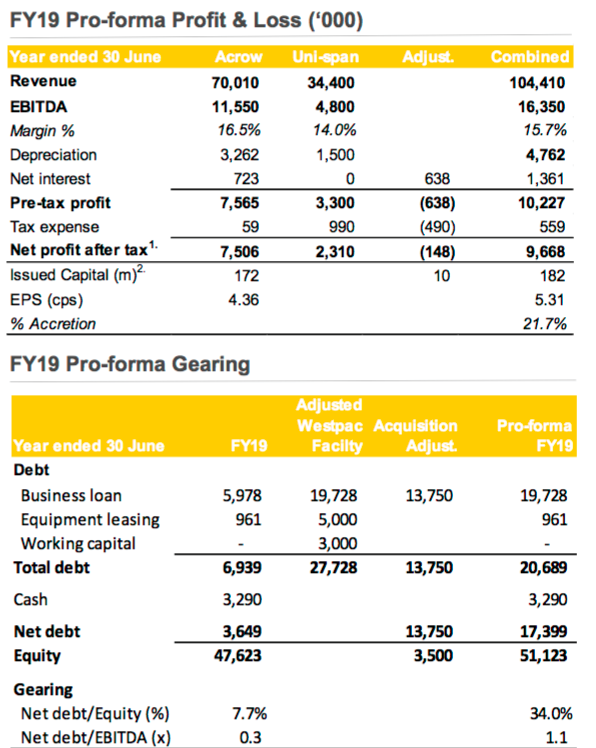

Acrow’s acquisition of Uni-span (a Queensland formwork, industrial scaffolding and labour hire company) for $21.25M (4.4X FY19 EBITDA) is a game-changer for the little-known $70M microcap. Uni-span primarily serves the typically defensive civil infrastructure market. The acquisition immediately adds 22% to EPS (from 4.36cps to 5.31cps) before any potential synergies are realised.

Potential synergies include revenue synergies from complementary products and services, as well as integration synergies with regard to yard consolidation, staff and other general expenses. Such synergies support earnings growth over the mid-term. With the business trading at 6.7X forward PE and 4.6X forward EBITDA, there is not a lot of growth priced in. The new consolidated group has already experienced early success with a 6-9 month $2.75M contract to provide formwork propping solutions for Sun Metals Zinc Refinery.

A particularly exciting part of Uni-span is its exclusive arrangement with ULMA (a leading Spanish manufacturer and supplier of formwork, shoring and temporary scaffolding systems). The newly consolidated firm recently signed a 3 year contract extension with ULMA, which now includes product distribution in New Zealand. Steve Boland, CEO of Acrow, stated that “We are encouraged by the similar dynamics being experienced in the New Zealand civil infrastructure construction market as those experienced in the Australian market at present. Early indications suggest that the marketing and supply of Acrow/ULMA formwork products into New Zealand will be well received by the market.” Uni-span also has a specific style of equipment which is key to tunneling-style work, further expanding the product offering of the combined business.

Acrow financed the acquisition with its Westpac facility, maintaining relatively conservative gearing of 34% net debt/equity.

In 2012, Warren Buffett purchased a WA crane company. In 2017, the company generated $6.15M of profit on revenues of $150M. It was a classic old-school Buffett investment… a founder-led, capital intensive, reliably profitable firm. Other construction companies owned by Berkshire Hathaway include: Acme Brick Company, Benjamin Moore and Co, Cavalier Homes, Clayton Homes, International Metalworking Companies, Johns Manville and Shaw Industries. Such businesses are not particularly glamorous but have relatively reliable cashflows and are easily valued on traditional metrics.

Insufficient Capital values Acrow Formwork at 7X forward EV/EBITDA (50% above the firm’s current valuation) based on discounted cash flow analysis and peer comparison.

5 Businesses on our CY2020 Watchlist

| STOCK | WHY WE’RE WATCHING |

| Bapcor (BAP:ASX) | Australasia’s largest aftermarket auto supplier/service provider (parts, accessories, equipment) with steady revenue, profit and dividend growth across its umbrella of brands. 5 year CAGR: Revenue +36% NPAT +42%, EPS +25%, DPS +18% Expansion to Asia (currently 5 Burson Auto Parts stores in Thailand) gives Bapcor access to far larger markets with the hope of replicating Australian success. At 18.1x consensus forward PE and 12x forward EV/EBITDA, the business is attractive if high single-digit growth can be achieved despite the underlying low economic growth environment. |

| Carvana (CVNA:NYSE) | Sells used cars online and provides finance for them. This means that they don’t have the typical costs and overheads of a traditional dealership. Cars are then delivered to your door. i.e. lower cost of doing business and more consumer friendly than traditional dealerships. Business has grown revenue organically at >100% pa but remains loss-making for now. Currently 0.4% market share in a highly fragmented market (with no single firm holding more than 5% of the market). If the business continues to demonstrate its value to consumers, market share could significantly expand. |

| Sandfire Resources (SFR:ASX) | Copper-gold producer valued attractively at a compelling EV/EBITDA of 2.5x with a strong net cash balance (about 25% of market capitalisation). We believe market has placed too much emphasis on its short mine life (~3 years) at its flagship DeGrussa project. SFR has made numerous investments in junior explorers, and a recent acquisition of MOD Resources, which we think should provide adequate project pipeline. That said, we need to be convinced of management’s ability to allocate capital before making an investment. |

| Synlait Milk (SM1:ASX) | With strong ties to A2 Milk (A2M), SM1 develops its assets to deliver quality New Zealand dairy products, with a particular focus on the high growth infant formula market. Exclusive supply rights to A2M, 5 year minimum supply agreement signed in 2018, A2M owns 17.4% of SM1. Question marks surrounding the longevity of SE Asian demand for Australian infant formula and dairy products, particularly after the Chinese acquisition of Bellamy’s in September. 17.2X forward PE and 10.1X forward EV/EBITDA with low double digit earnings growth is very attractive. |

| Xero (XRO:ASX) | We were most attracted to XRO when we first bought Afterpay in late 2017. At the time, we believed we had enough exposure to unprofitable high growth firms in the portfolio. 2 years have passed and we clearly made the wrong decision (the company’s valuation has nearly tripled). XRO’s simple accounting software continues to successfully expand across the US and UK, with ever-increasing economies of scale (as is typical of SAAS businesses). It is a high quality, net cash business, benefiting from the broader move towards accounting simplification. At a consensus 2021 PE of 180X and EV/EBITDA of 55X with top line growth of circa +35% and earnings growth around +60%, we believe XRO will do well but struggle to see a continuation of past returns with the possibility of valuation multiple compression… famous last words. |

We hope to record strong performance throughout the second half of the Australian financial year and look forward to keeping our subscribers updated. The founder has their entire net worth invested in this strategy. If you would like further details regarding our activities, we are always happy to discuss portfolio positions.

Best Wishes for 2020 and a very Happy New Year.