Happy New Year to our much appreciated subscribers. 2020 was a devastating year that we will all be happy to put behind us. The terrible events of the year, which continue to take the lives of the world’s most vulnerable, truly remind us of the relative unimportance of strong financial performance when one’s health is compromised. We hope that as the Covid-19 vaccine is gradually rolled out, that the world can return to some level or normality and that 2021 may be a fulfilling, healthy and prosperous year for you all.

Performance Figures

The portfolio rose +31.11% over the first half of the Australian financial year, outperforming the ASX200 performance of +13.69% by +17.42%. The top contributor during the half was Afterpay (APT:ASX)… yet again. There were no detractors during the half. The weighted average market capitalisation of our portfolio is $AU6.8 billion (up from $AU2.9 billion at H2 2020). The portfolio currently has 1.12% cash and is most heavily weighted to our ‘Structural Tailwinds’ strategy.

Quarterly Portfolio Changes

There were two key portfolio changes during the half. These were:

- Purchase of Redbubble (ASX:RBL)

- Purchase of BetMakers (ASX:BET) – Will be discussed in a future newsletter

Redbubble (RBL:ASX)

“Millions of new consumers have been exposed to online, many of them will continue to shop in this way. This is particularly true in the case of Redbubble because the content is created by hundreds of thousands of independent artists, it is ever-moving and always relevant. This is all made possible by an on-demand business model.” – Martin Hosking, Redbubble Co-Founder

What is Redbubble?

Redbubble (founded in Melbourne in 2006) is a leading global marketplace selling products with independent artists’ designs printed onto them, delivered from 41 fulfillment locations across the world. Unlike other ASX-listed e-commerce businesses, only 6% of Redbubble’s revenue is recorded in Australia. It is personally fulfilling to own part of a company which supports creativity.

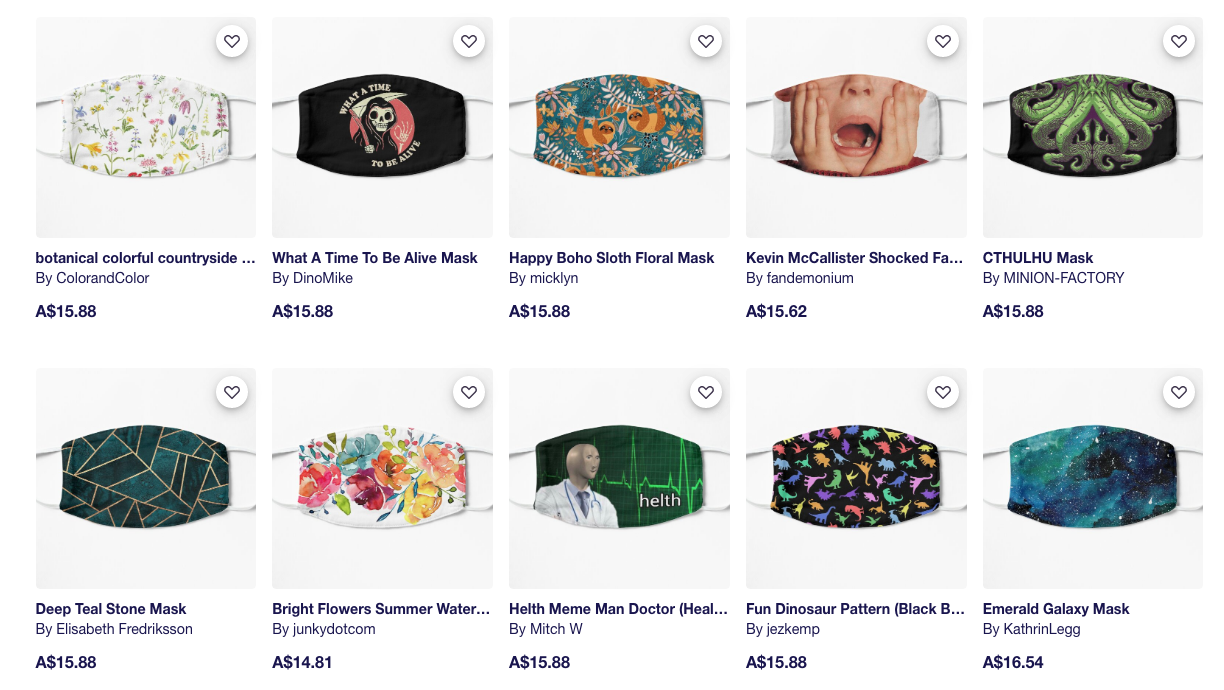

Redbubble’s unique structure allows artists to choose their own mark-up on base products, effectively controlling their ‘Artist Margin’. However, artists quickly discover the concept of price elasticity of demand and find a margin which maximises their revenue. As shown below, artists often copy each other’s Artist Margin and there is not a large price range.

Redbubble’s product offering is uniquely priced to benefit both artists and consumers, with competition amongst the 500,000+ artists keeping prices reasonable, whilst allowing the artist to have complete control over their margin. In FY20, artist revenue was $AU67.4M (16.2% of the total sales of $AU416.3M) i.e. Redbubble collected revenue of $AU348.9M ($AU416.3M-$AU67.4M) net of artist revenue.

Pricing Example:

T-Shirt Base Price $AU15 (cost of manufacture plus Redbubble’s gross profit margin) > Artist’s Markup 20% (the markup set and edited by the artist) > Artist Margin $AU3 (T-Shirt Base Price multiplied by Artist’s Markup = margin collected by artist) > Retail Price $AU18 (T-Shirt Base Price + Artist Margin)

Popular products include T-shirts, stickers, phone cases, and most recently, masks. Masks have been sold through Redbubble since April and have been promoted to their own website category. The company is clearly taking advantage of a short term spike in demand for masks due to COVID-19. This is a key tailwind for Redbubble since masks are becoming as much of a fashion statement as jewellery or handbags.

Whilst many may be quick to dismiss this surge as a fad based around Covid-19, we believe that the demand for face masks today is likely to seed future sales in other categories from returning consumers. Repeat sales already account for around 40% of Redbubble’s revenue. Redbubble is directing website space (masks are positioned prominently at the top of the website) and ad spending towards masks because that is currently the most in demand product category. It is not because the other areas of the business are struggling.

TeePublic Acquisition

Redbubble’s proposition as a leading platform for artists to monetise their talents and for consumers to source a broadening range of unique products looks unlikely to change given its step-change in scale. Redbubble’s 2018 acquisition of TeePublic for $AU41M (at a multiple of 12.4X EBITDA) has gifted the company with further economies of scale through additional distribution partners.

Significant Founder Ownership

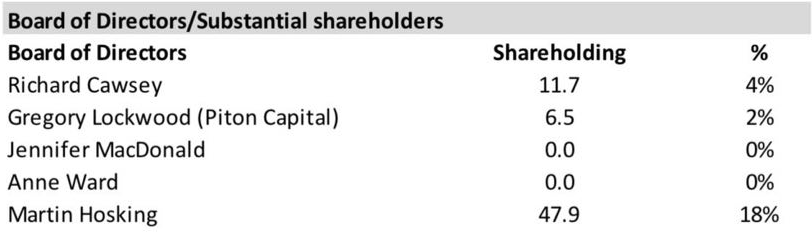

With technology firms trading at lofty valuations, one factor we look for to distinguish potential investments is a high level of founder ownership. At the end of FY20, Redbubble founder, Martin Hosking, held 18% of the company (although he recently reduced his holding to 16%). This high level of founder ownership is rare for an ASX-listed $AU1B+ capitalised company.

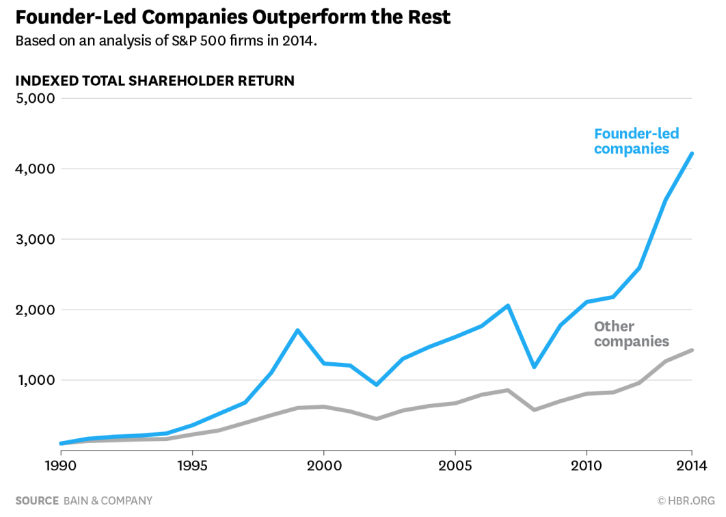

Founder-led S&P500 businesses have significantly outperformed their counterparts, driven by well-known consumer-centric brands such as Amazon and Facebook. In an Andreessen Horowitz blog, the firm outlines three reasons why founder-led businesses are the most attractive investment propositions. Founders typically have:

- Comprehensive Knowledge: exhaustive understanding and passion for the product, customer, business and market

- Moral Authority: willingness to abandon initial methods to challenge industry norms and continue to innovate

- Total Commitment to the Long Term: willingness to undertake long term strategic investments, which will help build a company that lasts longer than the founder

Whilst he is no longer the CEO (and thus, Redbubble is not founder-led in the true sense of the phrase), we are confident that Martin Hosking is truly dedicated to the continued growth of Redbubble’s marketplace and has no desire to step away from the business he founded.

Furthermore, we are confident in the ability of Redbubble’s newly appointed CEO, former SEEK executive (CEO of Asia Pacific and Americas), Michael Ilczynski. Michael and Redbubble entered into a non-recourse loan arrangement with a loan amount of $AU1,600,000. The loan plus $AU400,000 of Mr Ilczynski’s own funds will be used to purchase $AU2,000,000 of Redbubble shares on-market after the release of Redbubble’s H1 FY2021 results – such a financial commitment is far more than just a display of meek confidence for retail investors.

Positive Tailwinds

Participants in equity markets have recently realised that the triple digit revenue growth rates recorded by some e-commerce businesses cannot last forever (if you could double $0.01 every day for a month, you would have $5.4 million by the final day). Consequently, well-loved e-commerce stocks have sold off and traditional ‘old world’ value (e.g. banks, REITs, infrastructure) stocks have returned to vogue.

That being said, once COVID-19 is (hopefully) a distant memory, Redbubble will undoubtedly retain a proportion of customers who have purchased masks through retargeting of its highly engaged site visitor base (16 mins 11 secs average daily time on website). The 16 minute average daily time on site is comparable to social networking companies. The average visitor spends more time on Redbubble than on Twitter (12 mins 47 secs) and Instagram (8 mins 49 secs). Other e-commerce businesses record much lower site engagement (e.g. Kogan – 3 mins 42 secs).

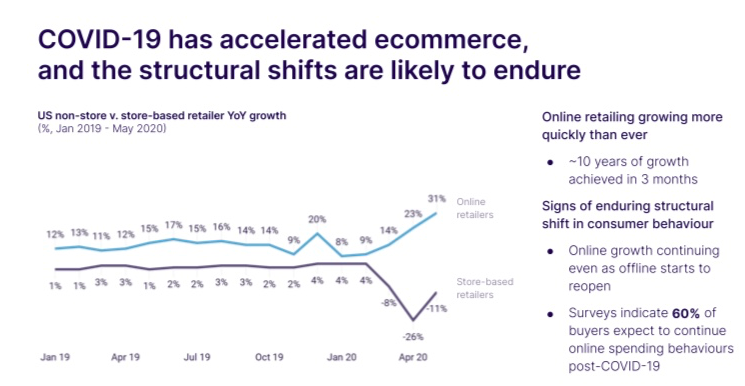

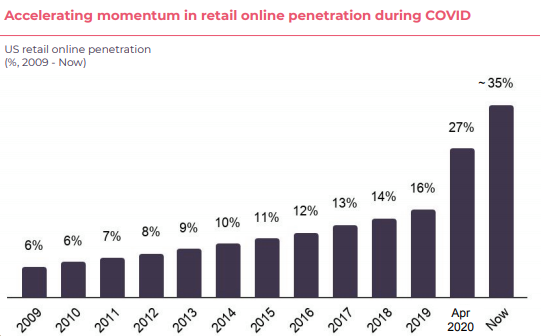

The other key (and more reliable) tailwind driving Redbubble’s sales growth is the COVID-induced structural shift towards e-commerce. Redbubble’s research reveals that COVID-19 has brought forward 10 years of online retail growth in just 3 months. Our other sources range from 5 to 12 years of growth over the period. People around the world have been forced to shop online and have realised that the experience is generally quick, simple and reliable.

Such digital shifts in behaviour are rarely reversed.

Customer growth has clocked in at 33%/annum over the last 5 years and has been achieved with pleasingly low costs of customer acquisition. Paid acquisition (Marketing) is astoundingly low, at only 10.2% of total revenue (Q1 2021, down from 11.4% over FY2020). In comparison, some of Redbubble’s peers spend up to 26% of revenue on marketing. Redbubble’s 511,000 artists are the company’s biggest voice, spreading the word about their online stores to bring customers to Redbubble free of charge – after all, it is in the artists’ best interests and represents a critical part of the company’s ‘flywheel effects’.

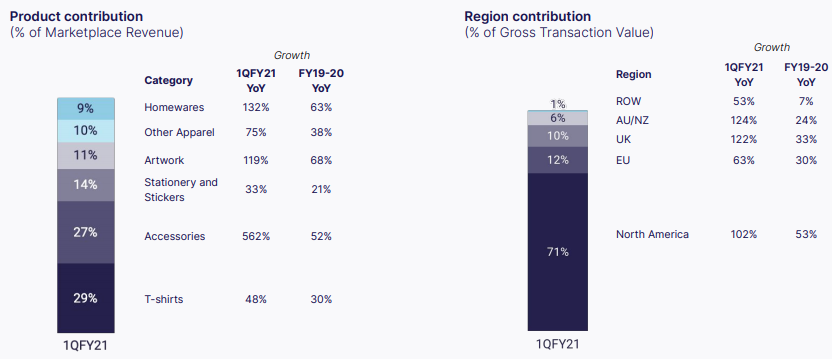

FY2020 Results

Revenue contribution by product and region is outlined in ‘Q1 2021 Results’. At the end of FY20, Redbubble had 511,000 artists selling on the marketplace (+51% on FY19), with 6.8M unique customers (+30% on FY19) making at least one purchase. The 51% uplift in contributing artists is a critical vote of approval for the marketplace, with more and more artists seeing the benefit of selling through Redbubble to generate income. The uplift has also been supported by another key tailwind – the evolution of the unconventional ‘side-hustle’, whereby many people (particularly Gen Z and Millenials) aim to generate a secondary income source outside of their main day to day job. This secondary income helps to support increased debt burdens for young adults across the world, whilst education, healthcare and residential asset prices have continued to increase faster than wages growth.

The growth in contributing artists is critical to developing Redbubble’s ‘flywheel effects’. There are three core elements of the flywheel:

- Artists and Content

- Loyal Customers

- Fulfilment and Operations

Redbubble’s capabilities, contributing artists and customers drive scalable 3rd party fulfilment across a global network of 41 fulfilment locations.

Real-Time Business Indicators

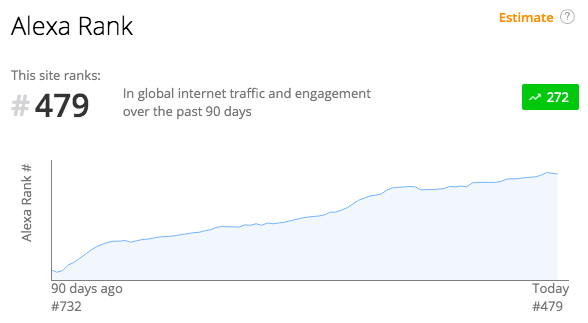

At Insufficient Capital, we monitor a myriad of real-time business indicators, particularly those relating to consumer behaviour. Trends give us a ‘feel’ for how a business is tracking long before its periodic quarterly/half-yearly updates to the market. We often use Alexa’s Site Overview tool to monitor global internet traffic and engagement for B2C firms. As at 15 October 2020, Redbubble’s website ranked #479 by global internet traffic and engagement (up from #732, 90 days previously – a phenomenal uplift in interest). There is a power law at play in site ranking, with each jump up the ranks becoming ever more difficult.

Q1 2021 Results

Redbubble’s Q1 results were nothing short of extraordinary, with the business effectively transitioning into rapidly increasing profitability (with high margins supported by well-targeted paid acquisition) as the business scales. The 43.7% gross profit margin recorded was the company’s best on record.

At the end of Q4 2020, masks represented 27% of total sales but fell to 14% by the end of Q1 2021 (still high but significantly less). This drop in mask contribution makes the overall Q1 revenue growth of 116% even more extraordinary. The ANZ region (6% of gross transaction value) was a stand-out, with growth accelerating from 79% yoy in Q4 2020 to 124% yoy in Q1 2021.

We are confident that future quarters will benefit from further customer acquisition and increased customer loyalty, alongside increased optimisation of the fulfilment network.

Valuation

We believe that Redbubble (RBL:ASX) is the last remaining pure e-commerce business on the ASX without a demanding ‘e-commerce valuation’.

The business currently (Q1 2021) has $AU85.4M of cash in hand and no debt. Management have not been in this cashed up position before and are still deciding on capital allocation, but have confirmed that they will not be returning capital to shareholders. We almost always support capital reinvestment policies and would generally prefer our portfolio companies to back themselves, just as we have backed them to allocate our capital. See below comparisons between Redbubble and other listed online marketplaces (although it is important to note that the comparables are not necessarily analogous). We believe that Redbubble’s ‘flywheel effects’ discussed above make it a superior (and more scalable) business to most of its comparables. Etsy is Redbubble’s closest peer and trades at a very rich 13.6X Forward EV/Sales. Kogan is the only peer trading at a significantly lower forward EV/Sales multiple than Redbubble, whilst eBay and Alibaba are the only peers trading at significantly lower forward EV/EBITDA multiples (however, both are growing slower than Redbubble).

If Redbubble’s FY21 marketplace revenue growth is only 49%, we would be very surprised. We expect closer to 60% growth, building off the phenomenal 116% achieved in the first quarter. We would love to own Redbubble for 3+ years as the firm’s marketplace continues to attract artists and customers.

We believe that Redbubble can grow revenues and EBITDA by 25%/annum over the next 5 years, benefitting from structural tailwinds and significant points of difference. We conservatively assume that there will be no further economies of scale contributing to margin expansion. In Q1 2021, gross margin expanded from 37.8% (Q1 2020) to 43.7%. Generally, on a sales multiple, we value Redbubble at 4X 2025 EV/Sales ($AU8.4 billion valuation = 5.7X today’s valuation as at 16 October 2020). On an EV/EBITDA multiple, we value Redbubble at 25X 2025 EV/EBITDA ($AU7.1 billion = 4.8X today’s valuation as at 16 October 2020). Both basic back-of-the-envelope valuations yield >35%/annum returns over 5 years.

What Could Go Wrong?

Whilst there are many risks to the success of the business, in the interests of attention span, we will discuss only litigation (a unique risk specific to Redbubble). Redbubble’s role as an intermediary for user-generated content exposes them to litigation risk as a result of intellectual property infringement. Currently, Redbubble will only review designs when someone submits a takedown notice. Another way Redbubble is addressing this issue is through their Partnership Program, which is a licensing agreement with rights holders. There are currently 67 content partnerships to promote the integrity of hosted content.

There have been some favourable decisions including recently in the United States, a clear vote of approval for Redbubble’s business model and IP enforcement procedures and mitigation strategies. However, litigation regarding IP rights is inherently uncertain and laws in certain jurisdictions could change unfavourably.

Performance of our Corona Watchlist vs the ASX300

In the depths of the coronavirus-triggered market correction, we put together a ‘Corona Watchlist’ of potential investments, which were discounted by the market panic. The watchlist’s 11 constituents were our key areas of research during the correction. Our Corona Watchlist and its performance as an equally weighted index are available here.

Cadence Capital is the only Corona Watchlist member which has been added to our portfolio. We outlined our thesis for Cadence Capital in our end of financial year newsletter. As an index, the watchlist has outperformed the ASX300 by +34.6% since 31 March (2.17 times the ASX300 index return of 29.5%). The weighted average market capitalisation of the watchlist is >$AU20 billion. The best performing stock in the watchlist has been Resimac, a premier non-bank lender, which is up 260%. In contrast, Charter Hall Long WALE REIT, a diversified REIT, has been the worst performing stock in the watchlist, gaining only 5.2% since March 31 as uncertainty regarding the future of commercial property (offices and traditional retail stores in particular) continues to loom over the entire sector.

Two additional watchlists are available on our website: ‘Microcap Watchlist’ and ‘International Watchlist’. The International Watchlist has performed particularly well (+82.4% since March 31), outperforming its benchmark MSCI World Ex-Australia Index (+18.2% since March 31) by 4.5X. Interestingly, only 1 of the 20 stocks on the watchlist are down over the period: Bank of China. Alpha Bank and Unibail-Rodamco Westfield have also performed particularly poorly – all three are old world stocks in a brave and competitive new world. In contrast, Carvana and Tesla have both more than quadrupled in value since March 31 – new world autos winning an old world industry.

Quip of the Quarter

“Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.” – Paul Samuelson, America’s first Nobel Prize winner in economics.

There is no doubt that market sentiment has significantly shifted from the deep fear of the March lows (and, just like every other market crash, the world did not end) to whispers of euphoric greed recently. Whether capital is flowing into the latest hot IPO, Buy Now Pay Later or ‘cutting edge’ medical opportunity, there is no doubt that vast amounts of cheap capital are sloshing through the bourse. The dichotomy between hot and not has never been greater. Financials and REITs have languished for the past 6 months, whilst tech and healthcare dash through prior highs. In time, there will be a great many ‘A-Ha Moments’, with some traditional ‘value’ stocks trading much higher. We hope that we own a couple of these unloved opportunities, with some investors continuing to behave like restrictions have been lifted at The Bellagio.

If you would like further details regarding our activities, we are always happy to discuss portfolio positions. We encourage you to follow us on Instagram and Twitter, where we share more regular bite-sized commentary.